Newly published research on the outcomes of last year’s controversial Job Ready Graduates funding reforms was reported last week in the Australian Financial Review with the headline: The big steal: why the government can’t deliver on uni places.

As AFR puts it: The analysis by Mark Warburton, an honorary senior fellow with the Centre for the Study of Higher Education at the University of Melbourne, argues that at the time of the Job-Ready Graduates legislation being passed last October, the “public and Parliament were told that there would be an extra 27,000 domestic student places this year … The reality of the JRG is that the government hasn’t provided the level of subsidy over the next several years to create the promised extra student places to support Australia’s economic recovery. The rhetoric of JRG is hollow.”

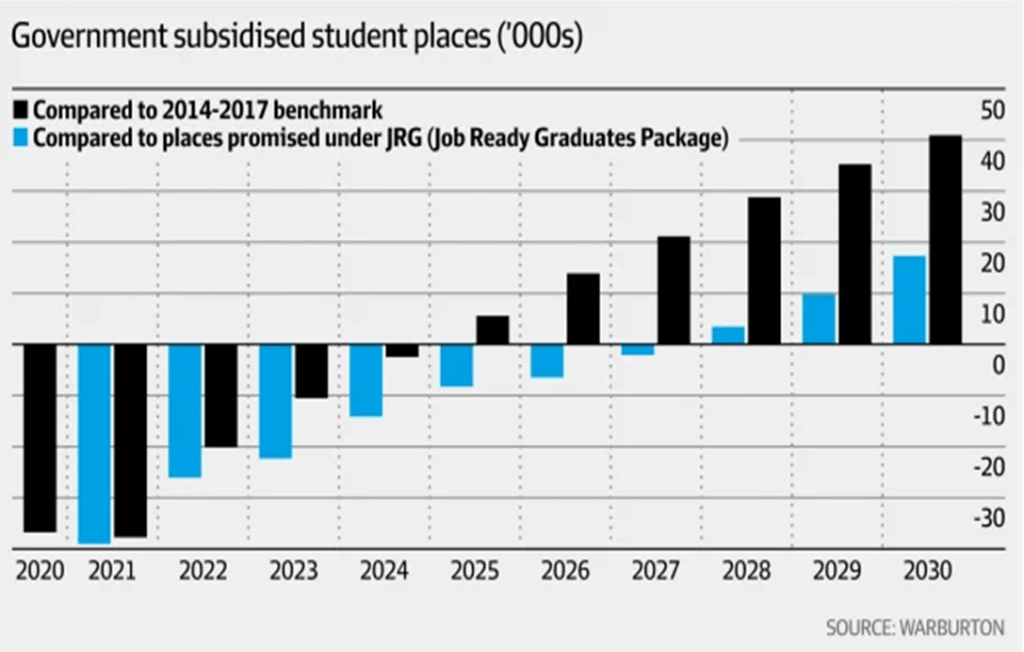

“The big steal: why the government can’t deliver on uni places” (Data source: Warburton)

Outlining his critique in The Conversation, Warburton writes: the total amount made available isn’t enough to provide subsidies for any extra student places, let alone the extra 30,000 this year announced by Treasurer Josh Frydenberg in his budget speech in May.

The full paper is on the MCSHE website. It examines past and present Commonwealth subsidy levels. It traces a series of government statements to Parliament last year, to support the JRG changes. It then compares the latter (the rhetoric) with the latest funding agreements for 38 universities for 2021-2023 (the reality). In sum: One year ago, the Government legislated major changes to higher education funding arrangements … At the time, it was believed there were slightly more than 626,000 Commonwealth supported student places (CSPs) in Australia’s higher education system. The public and the Parliament were told that there would be 27,000 extra domestic student places this year …

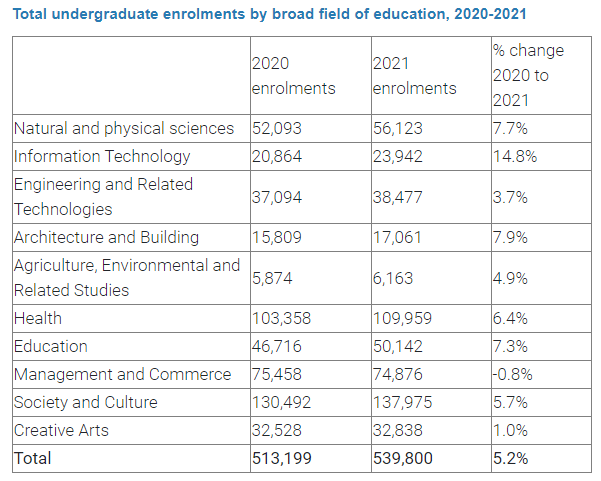

To aspiring students the issue here must seem simple: How many domestic students were enrolled in 2020 and how many are now, in 2021?

From a 626,000 baseline a rise of 4-5 per cent would amount to 651,000-657,000 CSP enrolments this year. That is, 25,000-31,000 more than in 2020.

In early 2021 the signs were positive. A media report in February cited several universities reporting that their domestic student applications were higher than in early 2020. A statement in March from Education Minister Alan Tudge presented data from 25 universities (Exhibit 3):

Early data from universities shows over 26,000 more Australians are set to study at universities this year … Data provided by 25 Australian universities shows a five per cent increase in total enrolments compared to the same period last year … Final enrolment data will be available later in the year when data for all universities has been submitted and validated.

25 March 2021 (for 25 universities)

If all 38 CSP-eligible universities average a 5% rise in domestic undergraduate enrolments, the 2021 target would be met. However, it’s possible that the 5.2% lift in Exhibit 3 has slipped back since March. The Minister’s statement on “early data” appeared a week before the cut-off date at which students may withdraw from courses without financial penalty (the HELP debt that covers their course fee). It’s possible too that 13 other universities not included in this “early data” have seen flat or falling enrolments. And as the Warburton paper notes, the Education Department has not yet reported final numbers for 2020. (Let alone 2021).

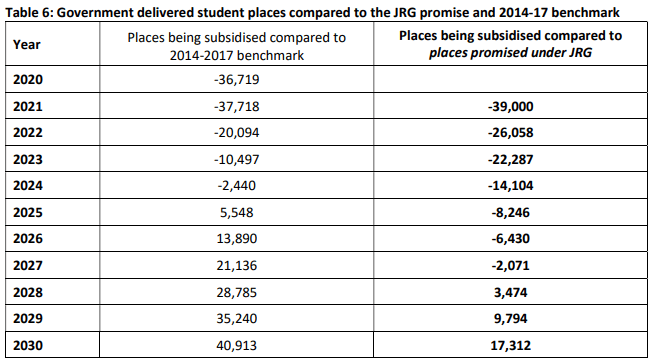

However the paper doesn’t refer to the March statement. Nor does it estimate how many more CSP students there are this year. Instead it recounts that last year’s JRG growth estimates assumed over 626,000 Commonwealth Supported Places (CSPs) in the system in 2020; and that later reporting found over 627,000 in 2019. Despite its conclusion that last year’s promise of extra places this year is hollow rhetoric, the number of CSP students in 2020 and 2021 is not the main focus of the paper. Its concern is that the full 38 university funding agreements don’t show enough grant subsidy money to fully fund 27,000 more places. And further, that accumulated grant funding shortfalls since 2018 translate to 39,000 fewer subsidised places in 2021.

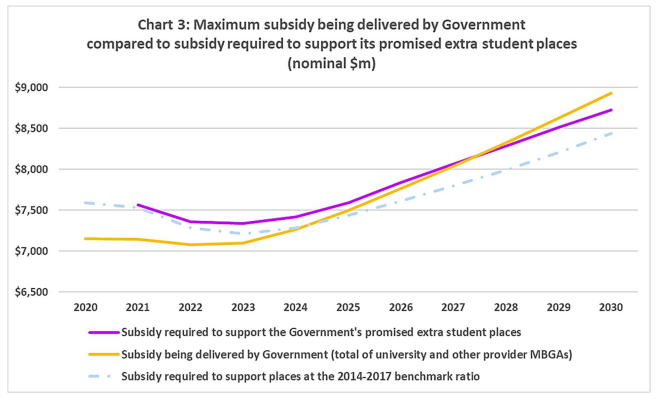

Compared with a “benchmark” rate of enrolment last reached in 2017, Warburton finds a CSP shortfall (equivalent to nearly 37,000 course places) already in the system in 2020, before JRG was introduced (Exhibit 4). This subsidy shortfall grew to nearly 38,000 places in 2021 (as the Australian Financial Review report shows in Exhibit 1).

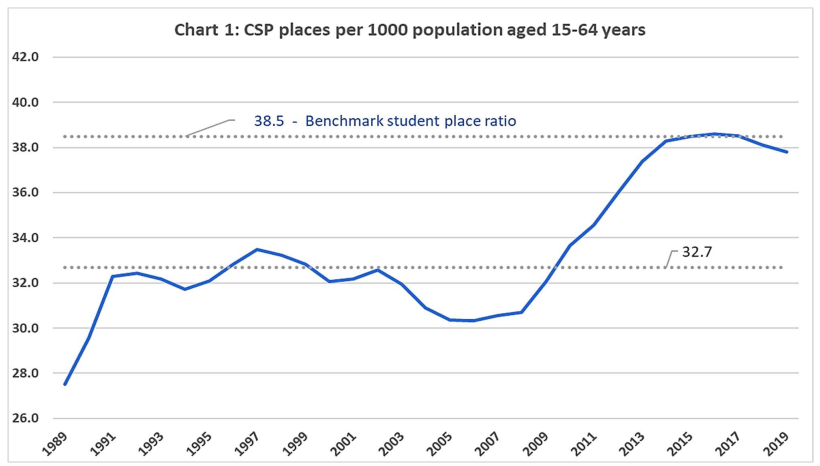

The basis for these benchmark estimates is the total number of CSPs as a share of the Australian working-age population over the period 2014-2017. (As seen in Exhibit 5, this was the peak reached after years of “demand-driven” funding policy. Under that policy, uncapped Commonwealth funding would rise to cover as many domestic students as universities were able to enrol).

According to the benchmark (38.5 per thousand 15-64 year olds) there could have been nearly 644,000 CSP students enrolled and fully funded in 2020 (see Exhibit 6), had demand-driven funding not ended. (Not the 626,000-627,000 on which JRG growth estimates were based.)

On this basis Warburton estimates the grant subsidy dollars universities have missed out on since the government decided to cap teaching grants from the start of 2018. The effect was to “freeze” grants at their 2017 level. This set the maximum level of direct subsidy for courses across the sector, even if universities offered extra places to meet further student demand. But it didn’t freeze the fee revenue paid by government on behalf of students via HELP loans. As with JRG settings for 2021, this remained uncapped.

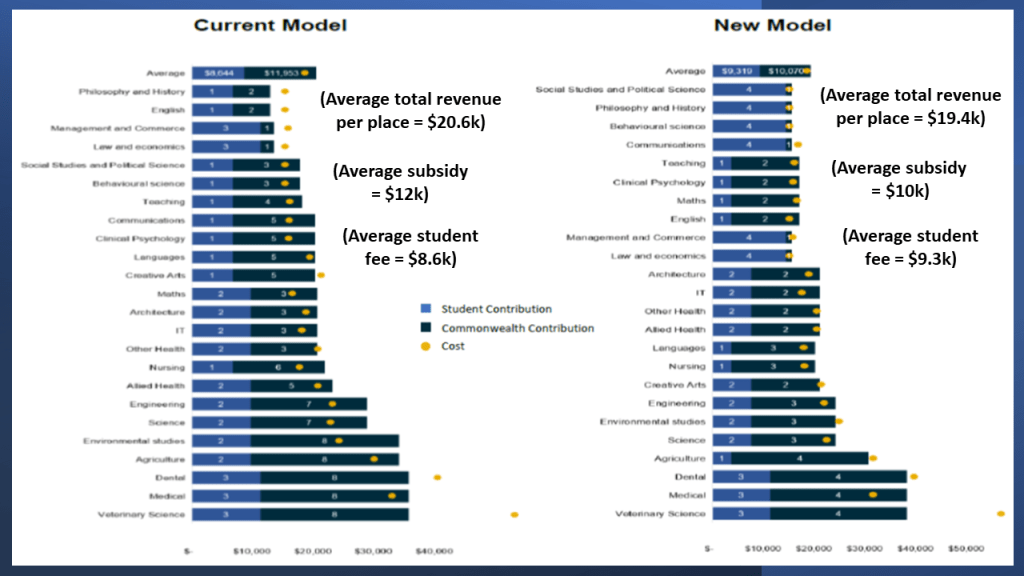

(The revenue effects here are complex. In practice, an extra fee-only place can earn a little less or a lot less than a subsidised one. Pre-JRG, domestic student fees this year would range from less than $7000 a year in Education or $10,000 in Science, to over $11,000 in Management / Commerce. Subsidy levels would range more widely from over $2000 in Management / Commerce, $11,000 in Education, $19,000 in Science or Engineering. For a university with unmet student demand, adding fee-only places in Management / Commerce looked viable in 2018 as they earned over 80% of the full amount. But in Science or Engineering they’d earn only 33%. However post-JRG fees in Management / Commerce are $14,500 per place – more than the 2020 fee and subsidy combined. In these fields – as in Humanities, where post-JRG fees are now just as high – fee-only places are more viable in terms of revenue per place than on a fully-funded basis in 2020 (see Exhibit 7).

As Andrew Norton said of these fields last year: In effect, these rates semi-restore the demand-driven system the government ended in 2017…

But again, only if there’s unmet demand for extra places. The Education Minister’s March 2021 data (Exhibit 3) shows no sign of growth in Management / Commerce fields. This, despite the fact that these fields normally attract high volumes of international students, and are likely to have seen pandemic-related declines. It is possible that with JRG fees now far lower in fields such as Education and Health, more students have opted for those fields in 2021 as the JRG changes assumed – but without greatly expanding total CSP enrolments beyond 2020 levels. Only time will tell.)

Returning to the Warburton paper, it recounts that under demand-driven policy, total CSP places rose from 597,000 in 2014 to 623,000 in 2017. Then more slowly over 2018 and 2019 (to over 627,000), due to the freeze. And as Exhibit 1 shows, post-JRG funding doesn’t redress the shortfall, which persists until 2025. Thus the paper’s conclusion: History will judge much of JRG to be a ruse to achieve the objective of increasing student contributions and lowering government subsidies. It is quite disingenuous of the Government to have ended the demand driven funding system, withdrawn subsidies for student places through the CGS (Commonwealth Grant Scheme) freeze and then claim it is helping Australians by taking until 2025 to restore to them the same opportunity to get a higher education that they had from 2014 to 2017 … The reality of JRG is that the rhetoric of creating extra student places to support Australia’s economic recovery over the next several years is hollow.

The “vibe” here is clear. Since 2018, government decisions have left courses under-funded and so left thousands of prospective students out of the system. And while thousands of extra places were promised this year, the government hasn’t delivered them. As an MCSHE post on LinkedIn puts it: one year on from the Government changes … The rhetoric of JRG has proven to be hollow, with research indicating there has not been the touted increase in student places … If the Government was to honour the claims it made to the public and the Parliament, it would need to provide around $1.1 billion more in subsidy from 2021 to 2024.

However the paper’s use of this “benchmark” to estimate funding and enrolment shortfalls is questionable. It assumes that the peak rate of CSP student enrolment seen in 2017 under demand-driven funding should have been a government funding target ever since: From 2014 to 2017, the number of subsidised student places grew … from 597,000 to 623,000. The system was relatively stable in size compared to the working age population. As highlighted in Chart 1, it was providing around 38.5 student places for every 1,000 people of working age during this four-year period. This will be referred to as the 2014-2017 benchmark ratio throughout this paper…

A number of objections may be made. First, no government has ever promised to fund this rate of CSP enrolment on the demand-driven funding settings that applied in 2017. To do so would imply an endless expansion in student numbers and funding, but no economies of scale in the delivery cost per course place.

(As I read it in July last year, the initial JRG plan aimed to align total funding per place to newly estimated course delivery costs; reduce the public subsidy per place; and pass more of the cost to students (see Exhibit 7). The net effect would be to finance enrolment growth of 6% by 2023 by an equivalent reduction in total revenue per place (offset by transition funding and other spending programs): First, it lifts student fees from $8.6 to $9.3k and lowers grant subsidies from $12 to $10k (on average, per year). Second, a planned 6% growth in enrolments (39,000 by 2023) is financed by way of a 6% fall in total funds per place, from $20.6 to $19.4k (on current profiles, which the plan aims to alter) … The cost of growth is met by students paying more (with HELP) and universities getting less per place … Fourth, these shifts allow the government to redirect Commonwealth Grant Scheme savings into other parts of the package …)

Job Ready Graduates – Higher Education Reform Package (24 June 2020)

A second objection is that the benchmark is a funding-driven view of course capacity and enrolment volumes. So by 2020, on this view, the 2018 funding freeze had led to nearly 37,000 fewer subsidised CSPs. This implies (as the paper’s point on restoring opportunity makes clear) that lack of funding left significant student demand unmet.

But at the end of 2018 it was reported that despite the freeze, 16 of the 38 public universities increased their offers of a place (while 13 reduced offers); and that demand that year was weaker overall, with over 14,000 fewer student applications (-4.1%) than in 2017. At the time sector experts – Warburton included – said the freeze hadn’t caused the decline. A year later, Andrew Norton concluded that the freeze wasn’t the main reason for falling enrolments in 2019: The issue is weak demand more than reluctant supply. Noting that most new demand comes from school leavers, Norton pointed out that Year 12 student numbers were lower in 2018 than in 2017, with little growth expected in 2019 and 2020.

A third objection to the benchmark is that (while funding levels do play a major role) governments don’t deliver course places. Universities do, in line with their own program and budget profiles, market positions and growth strategies. The mix and volume of course offerings – and of domestic and international enrolments – can vary widely.

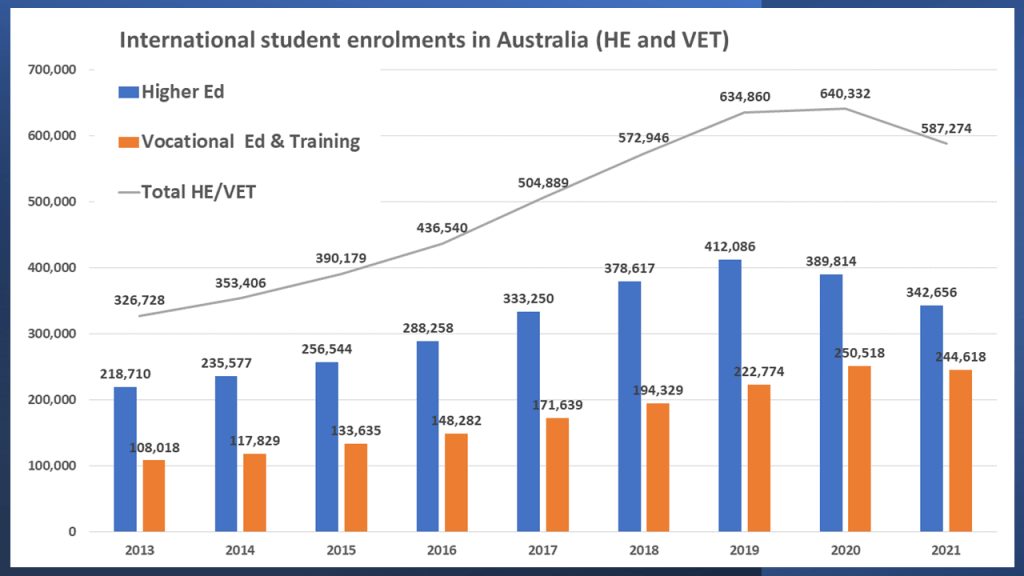

The Warburton paper recounts how domestic enrolment growth rates slipped after 2017 as teaching grants were frozen over 2018 and 2019. As noted, overall demand was lower in those years. And where there was demand, uncapped HELP loans gave universities scope to “over-enrol” CSP students for the fee alone, in some fields at least. But Exhibits 8, 9 and 11 indicate that many universities didn’t need to do this. Over 2018-2019 the sector added around 79,000 more international HE students.

(An international full-fee place earns no public subsidy. But the fee itself may be 2-3-4 times higher than the relevant domestic fee; and is often twice as high as the CSP fee and subsidy combined. In lower-cost fields – see Exhibit 7 – this makes overseas students far more lucrative per course place than domestic students, if the market demand is there).

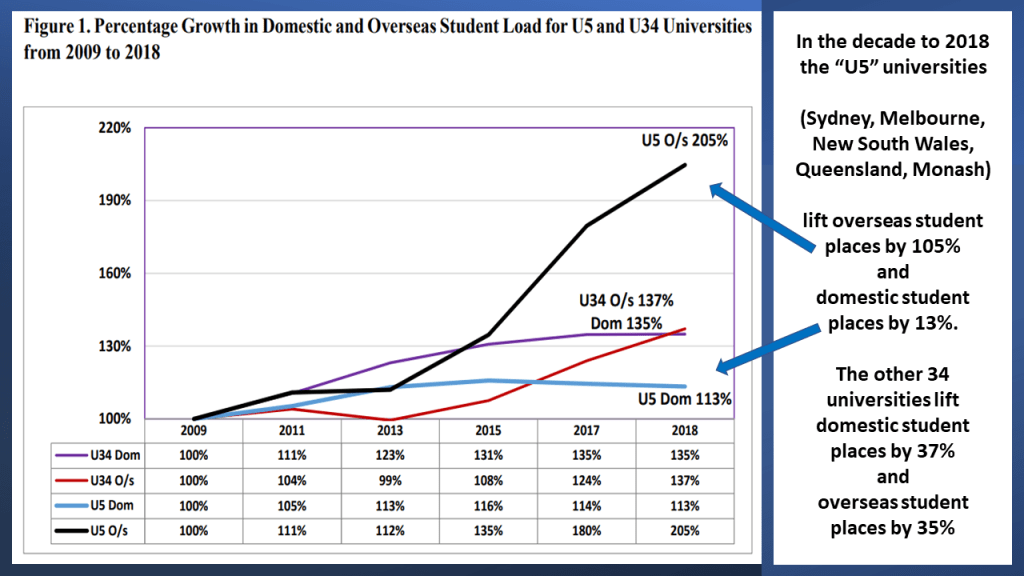

The revenue incentive to recruit international students instead of domestic ones can be seen in the growth strategies of the five largest Group of Eight universities. As MCSHE’s Frank Larkins showed in a paper last year (Exhibit 9): The U5 group of universities – Sydney, Melbourne, New South Wales, Queensland and Monash – in their quest for revenue growth have all profoundly changed the balance of their student profiles between domestic to overseas students over the decade 2009 to 2018.

For these universities it made sense to reduce the growth of domestic student places between 2015 and 2017, before the 2018 freeze on demand-driven funding – and then to continue on this path. Their revenue growth and research capacity strategies were built mainly on rapidly expanding international enrolments. Sector-wide, the rate of increase in international student places from 2015 was higher than for domestic students before and after the freeze.

A fourth objection to the paper’s benchmark is that factors other than domestic student demand may affect the number of CSPs it sets each year as a target for additional funding. As seen in Exhibit 8, in 2019 there were over 630,000 international students enrolled in Australian HE and VET courses, compared to around 350,000 in 2014. If counted among Australia’s working age population, a 38.5 per thousand rate for the additional 280,000 would require over 10,000 more CSPs in 2019 than in 2014. Except that none of these international students, here to study on a full-fee basis, would be eligible for CSPs.

The paper’s analysis finds a domestic student subsidy shortfall of $419m in 2021 due to the combined effects of the freeze and JRG (Exhibit 10). Here, for a mix of reasons, it excludes $345m in transition funding advanced to universities in 2021, on the basis that much of this may be withdrawn if (for example) universities replace subsidy shortfalls with extra student enrolments. The paper also excludes $256m for short courses in 2021 (which are not funded in 2022 and 2023 in university funding agreements).

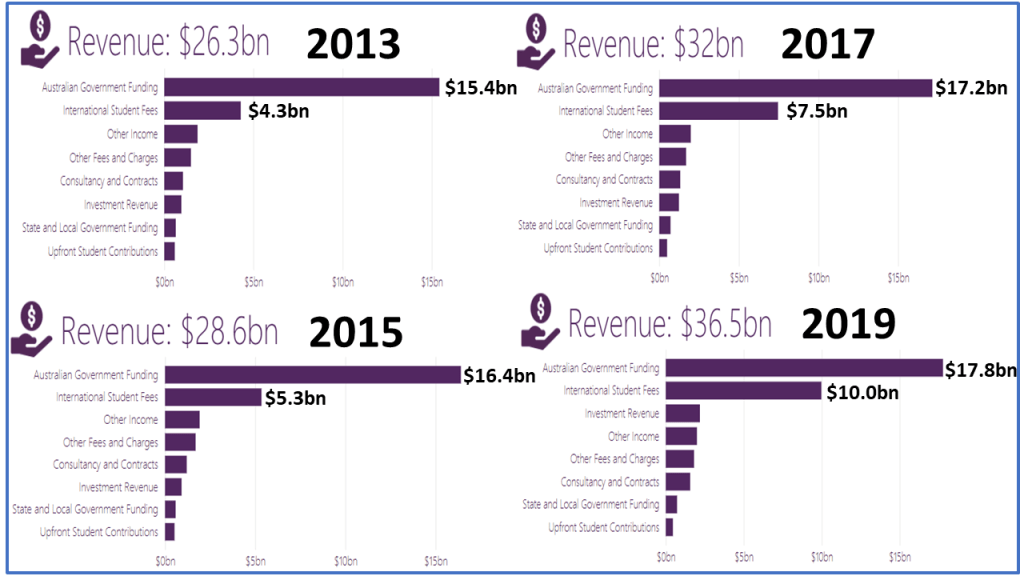

Even if we accept the $419m subsidy shortfall for 2021, this is not set in the sector’s wider funding context. The context is that total Commonwealth funding (including HELP loans) was about $18bn in 2020; and $19bn in 2021 in the May Budget speech. In turn, the Education Department’s current higher education finance publication shows the wider context of university sector revenue overall. Annual revenue from all sources grew from over $26bn to over $36bn from 2013-2019 (Exhibit 11).

In Education Department figures it is true that the growth of total Commonwealth funding (including HELP) slowed down over 2013-2019. It rose by $1bn over 2014-2015, then by $0.8bn over 2016-2017, then by $0.6bn over 2018-2019. But at the same time, total sector revenue rose ever more strongly due to rising international enrolments. It rose by $2.3bn over 2014-2015, then by $3.4bn over 2016-2017, then by $4.5bn over 2018-2019. The international student fee component rose by $1bn over 2014-2015, then by $2.2bn over 2016-2017, then by $2.5bn over 2018-2019.

By 2019 the sector’s $10bn exposure to international markets had set the stage for the pandemic-related budget crises unfolding since 2020. (As Exhibit 8 shows, in 2021 there are 69,000 fewer international HE enrolments than at their 2019 peak.) As a recent Mitchell Institute report explains, the large revenue shortfalls facing universities in 2021 are driven by pandemic-related border closures and declining international enrolments. (In 2020, the report finds a $2bn or 6% loss* sector-wide, with more to come in 2021).

When final domestic enrolment figures for 2020 and 2021 appear, areas of flat or falling enrolment in 2021 may as well reflect the disruptive effects of widespread campus lockdowns as the JRG changes to the student fee/grant funding model.

A fifth objection to the paper’s benchmark is that it defines opportunity for prospective students entirely in terms of their access to Commonwealth-funded course places in higher education programs. This ignores the collateral effects of demand-driven university funding on VET sector finances and course places in the five years to 2017. While a golden age of growth for HE enrolments (Exhibit 5), a 2018 Mitchell Institute paper shows that VET institutions saw sharp declines over this period (Exhibit 12).

In the end the paper’s conclusions use grant subsidy dollars as a proxy for the volume of course places; hence a proxy for more domestic enrolments this year; hence a proxy for future student access to HE courses as a share of population, and also a baseline for estimating shortfalls in student enrolment targets (Exhibit 1).

But since actual enrolment volumes in both 2020 and 2021 remain unknown, the paper cannot prove what it implies: the non-delivery of 27,000 more promised extra student places this year. By conflating the sector’s under-funding concerns with the wider question of domestic student access, the paper’s own rhetoric tends to mask this reality.

More funding always helps. And with further declines in international enrolment still looming, the sector will struggle to restore revenue from this source in the next few years. But for domestic students, access to what? This issue is best considered in the context of the tertiary education system as a whole. To do that would mean considering VET participation along with HE; and in turn the role of State governments in financing provision along with the Commonwealth.

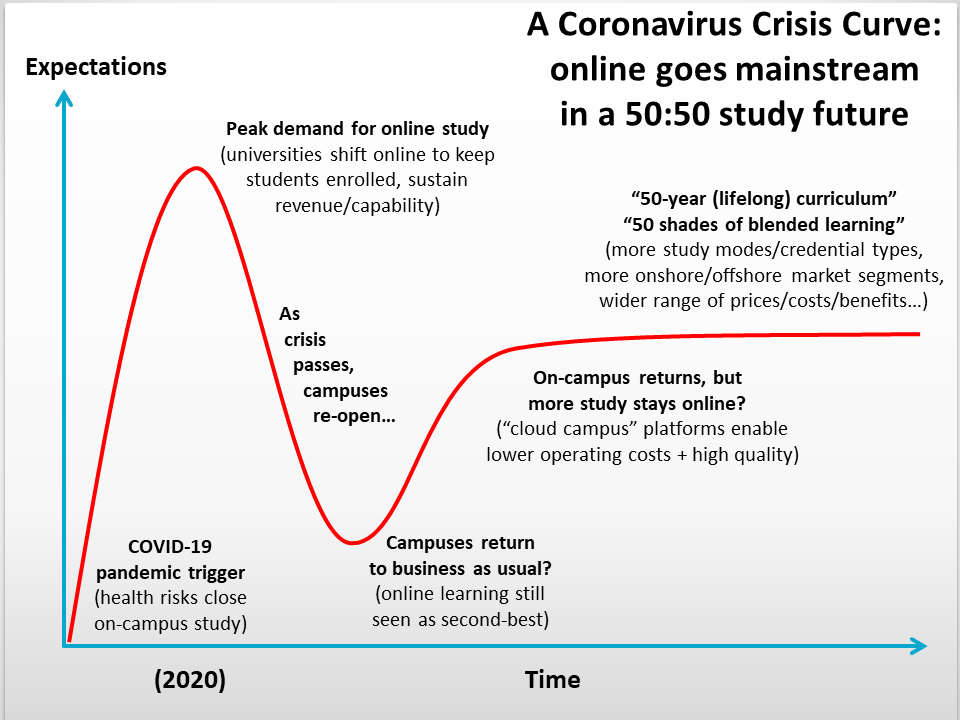

Arguably, open-ended demand-driven funding for Australian universities has had its day. Whatever the final number of domestic HE enrolments in 2021, reform is still needed to Australia’s tertiary system design. The design of what is now an evolving multi-platform system will shape what mix of programs, skills, credentials and pathways into future occupations are on offer in a “lifelong blended learning society” (Exhibit 13).

The issue of how best to fund and deliver all this will turn as much on system design as on levels of funding overall. The best approach to such a complex reform task, and the modelling needed to support it, is likely to come from a tertiary education commission, independent of governments and of the university and vocational sectors too.

In a post-secondary sector likely to see further transformation over the coming decade (as sketched in Exhibit 13), such a body may avoid the piecemeal reform efforts seen in recent years, and offer Australia better ways forward.

*A new report by MCSHE’s Frank Larkins and Ian Marshman puts the sector’s 2020 losses at about 5%, or just under $2bn.

Afterword

This analysis does not argue against further funding for universities. Nor does it support the JRG changes introduced last year. Aside from how much funding there is in the system, given its aims JRG does have design flaws. For example, it creates financial incentives for HE providers to enrol more students in fields that the government sees as lower-priority. And while not designed to offset international revenue shortfalls in 2020 (other one-off funding measures were taken), JRG assumed that borders would re-open at the start of 2021. When they didn’t, the government didn’t add further substantial one-off funding measures).

As noted in this blog last year, the Innovative Research Universities proposed a more workable set of funding model changes in August last year.

And for discussion purposes only, last year I sketched (but have not modelled) a possible alternative funding model with discounted student fees for online-only study.

Further reading

Peter Hurley, Melinda Hildebrandt and Sam Hoang, 30 August 2021, Universities lost 6% of their revenue in 2020 – and the next two years are looking worse

Mark Warburton, 13 September 2021, New analysis shows Morrison government won’t cover any extra student places for years

Stephen Matchett, 13 September 2021, Government funding more students – there’s a wait

Tim Dodd, 13 September 2021, Unis short-changed by $1.1bn in job-ready graduates scheme

Julie Hare, 13 September 2021, The big steal: why the government can’t deliver on uni places

Frank Larkins and Ian Marshman, 28 September 2021, The 2020 Financial Outcomes of Australian Universities within the COVID-19 Pandemic Environment

Andrew Norton, 7 November 2019, Enrolments flatlining: Australian unis’ financial strife in three charts

John Ross, 3 November 2018, Stuttering demand shows Australian funding freeze ‘unwarranted’

Geoff Sharrock, 25 May 2018, Six things Labor’s review of tertiary education should consider

Geoff Sharrock, 27 July 2020, Guest lecture notes on the 2020 higher education reform plan, Job Ready Graduates

Geoff Sharrock, 11 November 2020, Reforming Australian tertiary education: what did Clark Kerr do?