The 2020 edition of the OECD’s Education at a Glance report landed on 8 September.

In Australia it caused barely a ripple of public interest. With past editions, university sector press releases and media commentary usually appear within a few days. Typically, these highlight how low we look in the latest OECD “ranking” of tertiary sector funding.

Despite the strong growth seen in Australia in successive OECD reports, local myths persist about our sector’s funding history, and how we compare internationally. Echoes of these arise in 2020 commentary on the sector’s sudden exposure to sharp falls in international revenue.

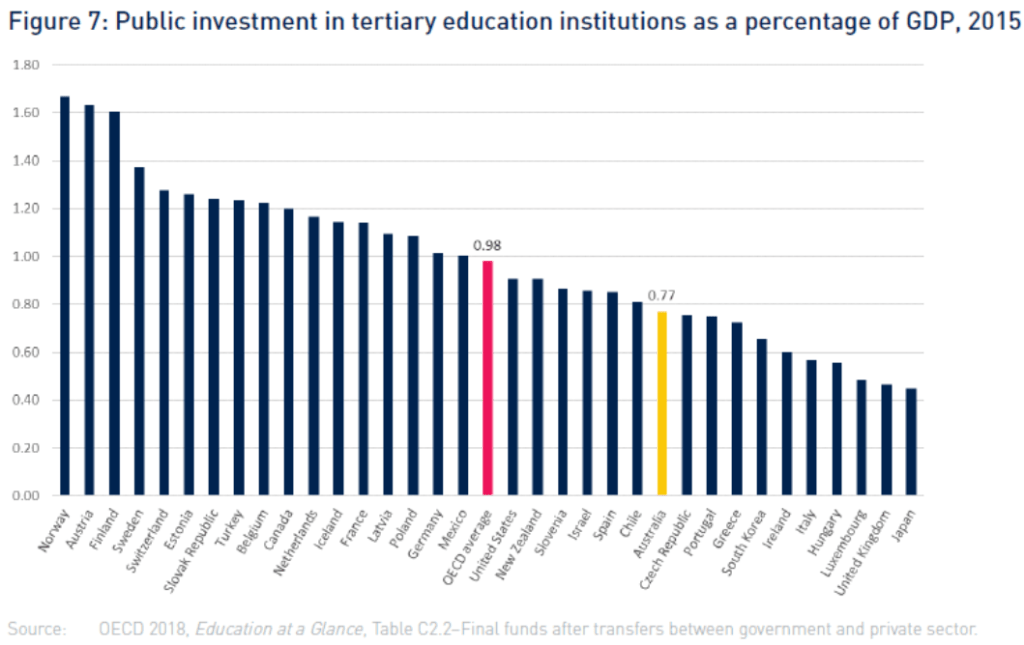

Some still refer to decades of declining government funding. Others, to the way diminishing levels of public support have left Australian universities badly under-funded relative to most in the OECD. And others, to a system based on falling public investment (now down to less than 40% of all revenue), offset by increasing dependence on international student fees. A recent Senate Inquiry submission on the government’s funding proposal from the National Tertiary Education Union framed our sector’s apparently severe under-funding in familiar terms: “Australia’s public investment in tertiary education (0.7% of GDP) is well below the OECD average (1.0% of GDP) and is one of the lowest amongst all OECD countries” (original emphasis).

In this narrative, most other OECD countries are assumed to provide better levels of funding, and/or stronger spending growth over time. As we look back from 2020, a local expert suggests, “the essential story of Australian universities over the past forty-five years (has been) massive growth combined with declining public investment”.

So again, it’s worth posting some charts to show how Australia has fared and compared for the last decade or so. Let’s start with total tertiary sector revenue as a share of GDP.

In 2017, peak body Universities Australia claimed that this had been “flat since 2000” while rising elsewhere in the OECD. However, our university sector revenue has doubled since then in domestic data; and it grew far faster than our GDP (Charts 3 and 5).

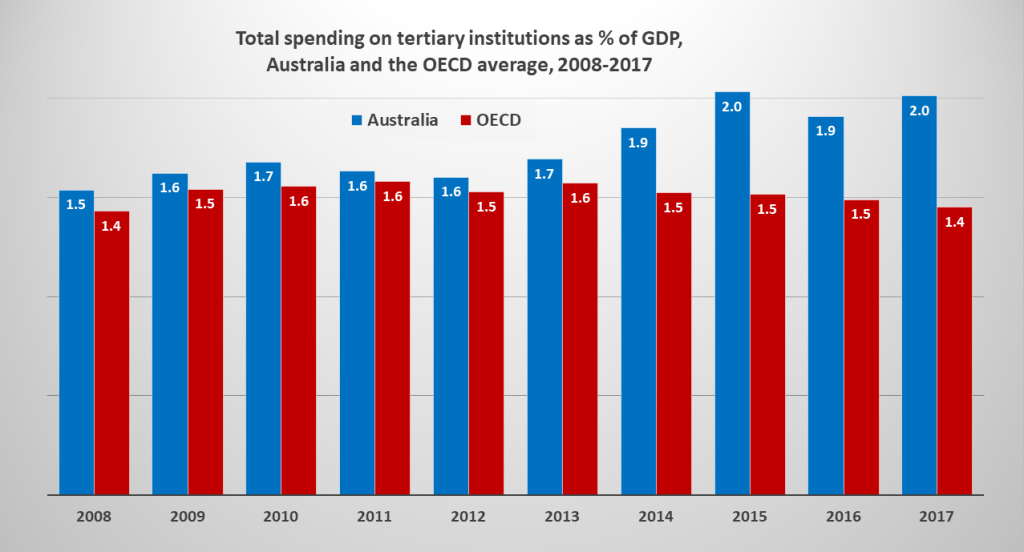

The (wider) tertiary sector’s growth is consistent with trends seen in OECD reporting. As Chart 1 shows, over 2008-2017 the Australian rate of tertiary spending grew strongly, from 1.5 to 2.0% of GDP. By contrast, the OECD average rate reached 1.6% in the years following the 2008 financial crisis, then slid lower to 1.5 and now 1.4% of GDP in 2017.

Chart 2 shows that in 2017, Australia’s rate for tertiary institutions (university degree and vocational diploma programs) was the fourth highest of 36 OECD countries. As explained in my June post on the OECD’s 2019 report, many European countries saw flat or falling spending after 2008. In 2017 the European Union average rate was 1.2% of GDP.

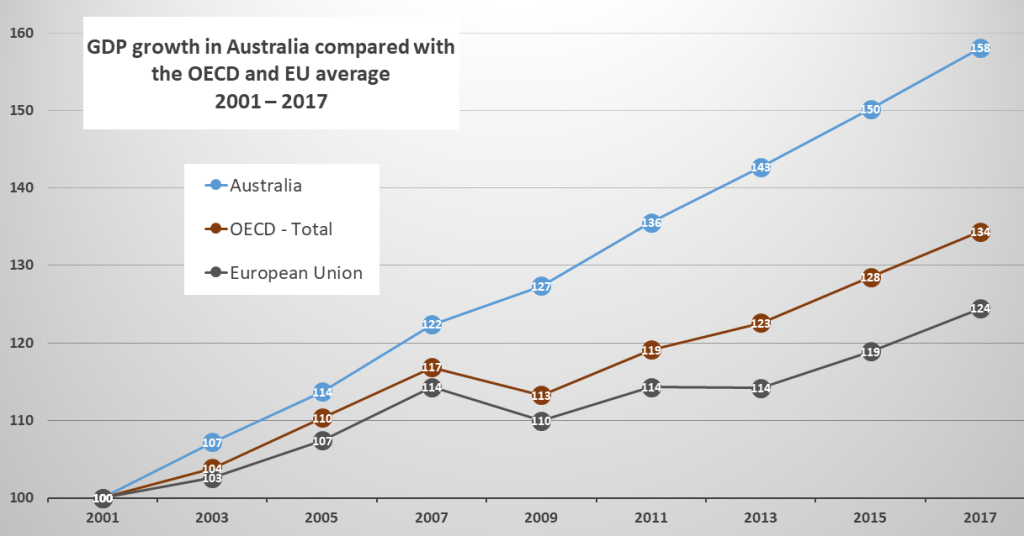

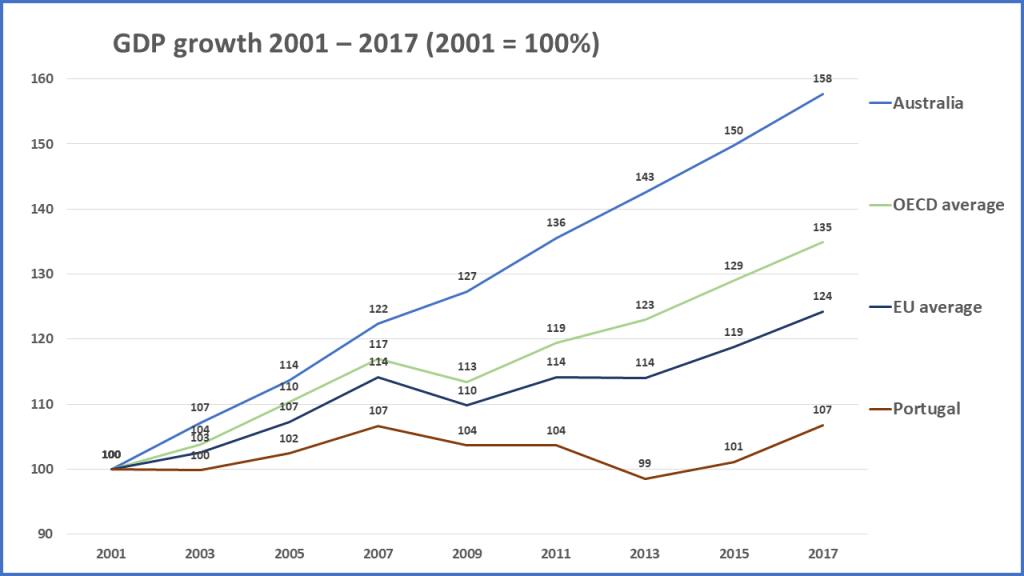

In fact, the revenue growth gap between our tertiary sector and those of many other countries is larger than Chart 1 suggests. Lurking behind the headline rates is Australia’s above-average GDP growth. As Chart 3 shows, it grew by 58% over 2001-2017, compared with OECD and EU averages of 34 and 24%. For a decade, our local commentary has taken GDP as a “common denominator” for OECD spending comparisons. (The main focus has been on “final” public spending – it’s hard to find anyone highlighting the 2.0% figure in Charts 1-2.)

While defended as “standard practice” to compare levels of public spending, relying solely on such metrics has predictably unenlightening effects. It masks the extent of real rises in Australia; and of flat or falling spending in countries with weak GDP growth, particularly since 2008. As the OECD noted in 2012, Australia is seen among OECD countries as an “Iron Man” of economic growth and resilience.

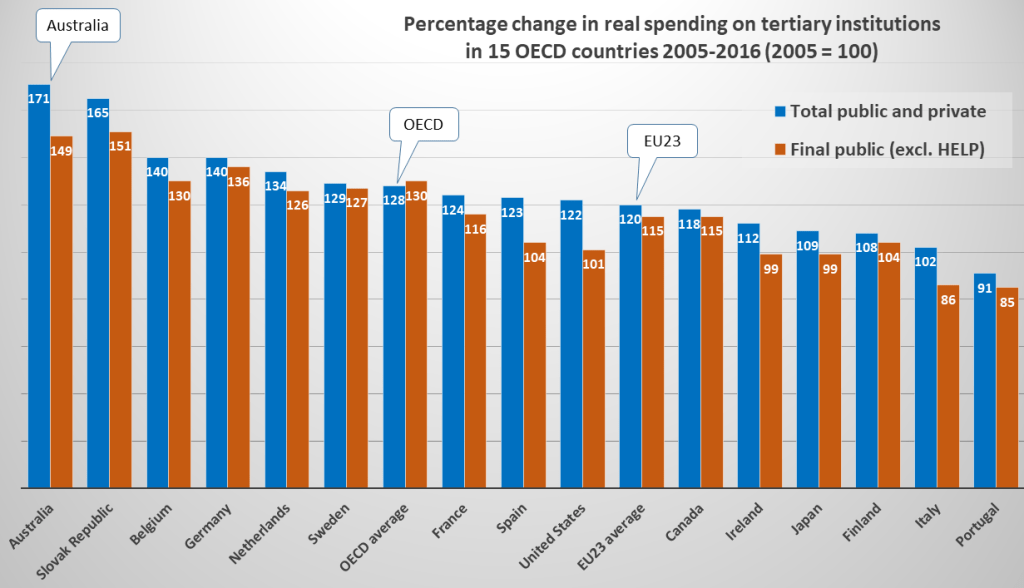

As seen in Australia’s 2008 Bradley Review, other OECD metrics shed more light on real spending trends. As I outlined in June, total tertiary spending rose by 71% in Australia over 2005-2016, in the OECD’s 2019 report. This compares with growth of 28 and 20% for the OECD and EU averages. In final public spending (excluding HELP loans) government funding in Australia grew by 49% compared to 30 and 15% for the OECD and EU. Chart 4 compares Australian spending growth with 14 other countries, for total spending and final public spending, in GDP-adjusted terms. These OECD metrics disconfirm the majority view found in Australia.

In local commentary, a common point of comparison is with final public spending in Nordic countries, as a share of GDP. Why can’t ours be more like theirs, where rates are far higher, and final public spending makes up more than 80 or 90% of total tertiary spending? In Finland for example, final public spending was 1.4% of GDP in 2017 (twice the Australian rate) where it accounts for over 90% of the sector’s revenue (Chart 7).

But part of the reason for this is that Finland has had below-average GDP growth. Over 2001-2017 its GDP grew by 23% (compared with 34 and 58% for the OECD and Australia).

Chart 4 shows that final public spending in Finland grew by just 4% over 2005-2016, and total spending by 8%. In the metrics that matter for resourcing, such as total spending per student, Australia looked stronger than Finland at the degree level, if R&D spending is included (and also Denmark, though similar to Norway, and not as strong as Sweden – see Charts 9 and 10).

The strong Chart 4 growth trend in the OECD’s Australian data is consistent with our own domestic data on university sector revenue. As the ANU’s Andrew Norton noted recently (July 2020): “the sector narrative of continuing government funding cuts is only sometimes true. Teaching subsidies were frozen from 2018, but after a decade of strong growth. Since 2001, total revenue for Commonwealth supported students has grown by 165 per cent in real terms”.

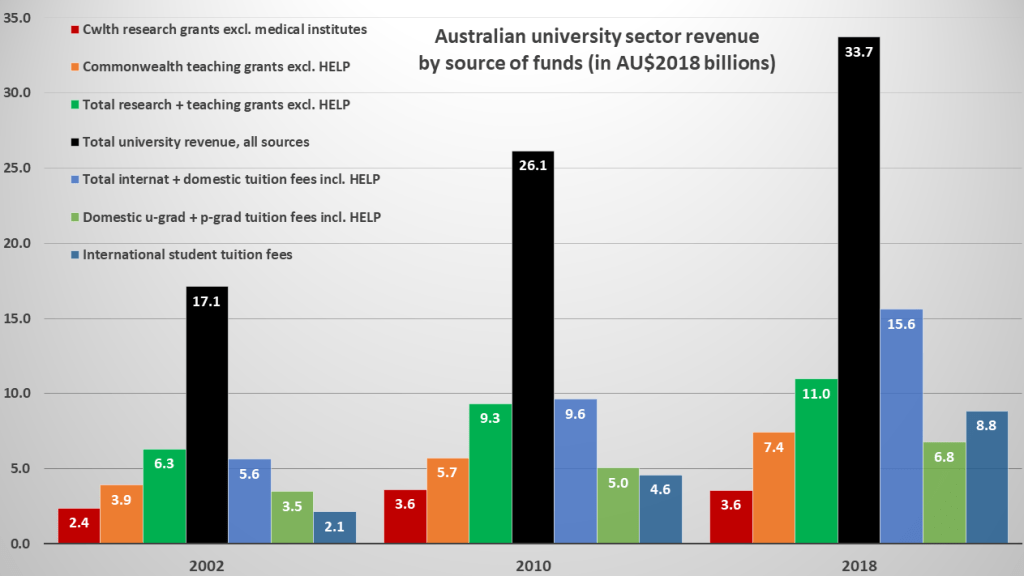

The domestic data in Chart 5 show total university sector revenue almost doubling in real terms from 2002 to 2018, to just under AU$34 billion. Commonwealth grant spending rose from $6.3 to $11 billion. From a lower starting point, HELP loan spending rose faster. And from an even lower starting point, international student fee income (the “secret sauce” of the sector’s revenue growth) rose much faster: more than fourfold to $8.8 billion in 2018.

While Australia’s GDP growth has been exceptional by OECD standards, it has not grown nearly as fast as sector revenue. On this view, to suggest that total tertiary spending has been “flat” since 2000 as a share of GDP looks like lobby group “gaslighting” (but may be an updating error of an older script).

The Australian folklore also reflects a conflation of the rising share of private spending with assumptions of flat or falling levels of government support. A related source of confusion is the widely held view that: “Where in 1989 universities derived more than 80% of their operating costs from the public purse, now it is estimated to be less than 40% – a figure well below the OECD average for public investment in tertiary education.”

Some commentators put today’s public share of funding at 35% or even 30%. But whether drawn from OECD or domestic data, this paints a partial picture of Australian university budgets, and how governments support them. In 2020 the Commonwealth has guaranteed $18 billion in funding to the sector, in grants and HELP loans. If this were 40% of total revenue, the sector would be earning $45 billion in 2020. If 30%, the total would be $60 billion. As Chart 5 shows, in 2018 total revenue was less than $34 billion.

In their focus on direct grants only, commentators overlook the public loans paid directly to universities by governments. This implies that, as a form of government support, HELP’s no help at all. But today’s international revenue crisis makes the sector’s dependence on every form of government financing more obvious. Recently, the University of Melbourne’s Frank Larkins and Ian Marshman put total non-government revenue at 46% in 2018 (i.e. the total government share was 54%). From a budget risk and jobs-at-risk point of view, total public cash-flow matters much more to the sector than which of the various Commonwealth funding streams provides it, or whether HELP loans are finally repaid through the tax system. Without public HELP financing, domestic student demand would falter in Australia, along with international demand.

As the ANU’s Andrew Norton points out, the government’s current plan to cut direct funding and lift domestic fees allows universities to expand enrolments in some fields, solely on the basis of “demand-driven” HELP loans: “The main growth potential created by the Job-ready graduates package is the prospect of a defacto demand driven system in the $14,500 student contribution fields of arts, business and law. Universities could ignore the $1,100 Commonwealth contribution and increase enrolments on the student contribution alone.”

Meanwhile, some 2020 commentators still recall that over 1995-2005 the OECD average growth in (final) public spending was 49%, compared to zero growth in Australia (as shown in the 2008 Bradley Review‘s only chart on OECD spending comparisons). But, as noted in June, the past decade of “decline and fall” commentary fails to recognise the big reversal ever since, in OECD reporting.

As I noted back then, the main reason is that, since Bradley, no-one kept tracking and talking about the trends seen in the metrics it had highlighted. Instead, the focus shifted to final public spending (excluding HELP) as a share of (post-2008) GDP. An example from Universities Australia’s 2019 Higher Education Facts and Figures report is shown at Chart 6. On this basis, UA has stayed on-message: “Australia’s public investment in tertiary institutions as a share of GDP was amongst the lowest in the OECD—ranked 24 out of 34 countries.”

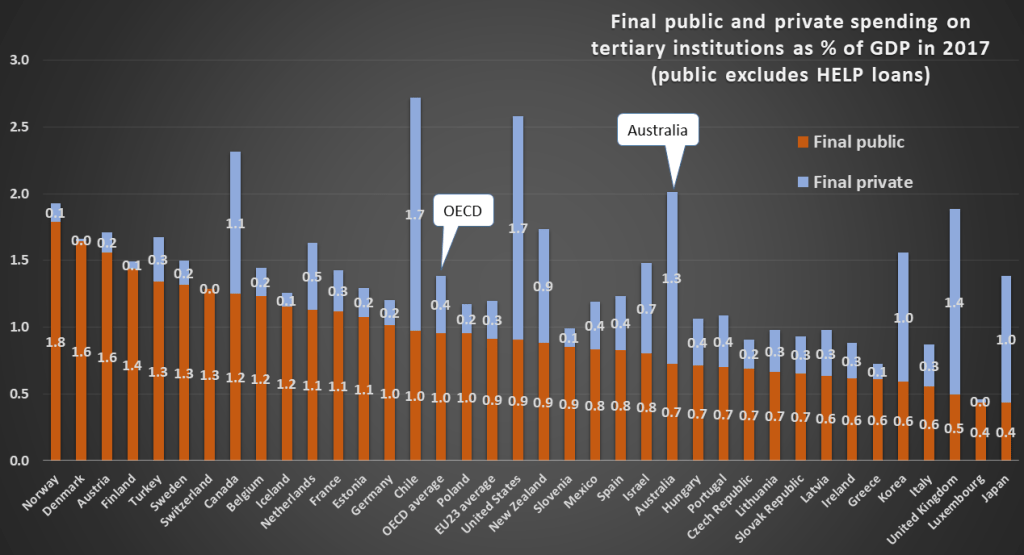

As noted, GDP growth disparities mask the reality in such comparisons, however precise a figure such as 0.77% may seem. (As one of the sayings about statistics goes, figures like these can be used to “draw a mathematically precise line from an unwarranted assumption to a foregone conclusion”.) And as I’ve pointed out since 2015, this kind of ranking doesn’t prove that our universities are under-funded. It’s a partial view of Australian realities, masked by GDP growth disparities and the way HELP loans are classed in some (but not all) OECD metrics. Chart 7 shows the same dataset from the OECD’s 2020 report with “final” private spending placed on top of “final” public spending. This highlights the gap between Australia’s 2.0% in total spending and the OECD average of 1.4 (Chart 2).

On the private spending side, it also reflects the boost to total revenue that Australia has enjoyed from international income in recent years, as seen in Chart 5. (Given the time-lag in OECD financial reporting, the big drop in tertiary sector revenue from this source during the 2020 pandemic won’t be seen in charts like this until the OECD’s 2023 report.)

Those who subscribe to the sector’s narrative tend not to dwell on how strong Australia’s total tertiary spending looks in most OECD metrics, relative to most others in the OECD (Charts 1-2).

The local habit of highlighting a “Chart 6 slice” of data was the basis for Universities Australia’s claim in its media release on last year’s OECD report: “Australia continues to rank near the bottom of the ladder for public investment in tertiary education – we won’t be able to compete with other advanced economies if this doesn’t improve”. This was also the basis for the NTEU’s assertion that this year’s OECD report still ranks Australia “one of the lowest amongst all OECD countries” for public investment.

But (to quote a former prime minister’s partisan quip) this is an “all tip and no iceberg” view of public financing. GDP disparities aside, the significance of HELP loans as a public financing instrument for the Australian tertiary sector can be seen in its domestic data. Over 2009-2018, unrepaid HELP debt rose from $18 billion to $62 billion.

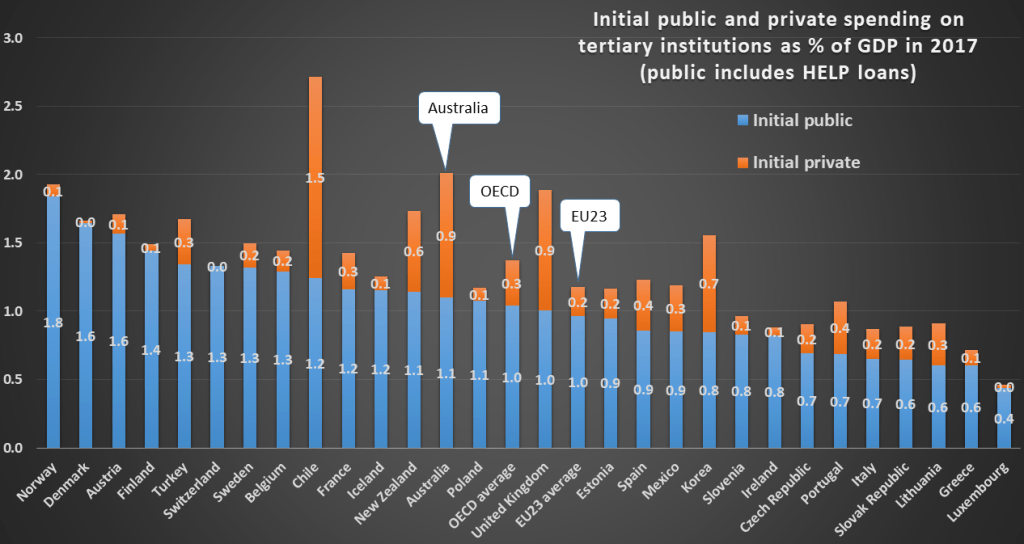

In Paris, meanwhile, the OECD is aware of the distorting comparison effects of public loan schemes. Its more recent reports highlight “initial” public spending, not just “final”. Chart 8 shows how this affects Australia’s “low-ranking” level (rate) of public investment. At 1.1% of (Australian) GDP in 2017, it was above the OECD average rate of 1.0%. And also above those of countries previously cited as examples of higher public investment (such as Spain, Mexico, Portugal).

Here it’s worth recalling that in 2017 (and even in 2018), local commentary assumed that our public funding was “second lowest in the OECD” (ahead of Japan). Such claims are duly accepted and reported in the media. As the vice-chancellor chairing the Group of Eight universities told sector leaders and policy reporters at the National Press Club in June 2017: “The government is already the OECD’s second-lowest contributor to higher education as a percentage of GDP”.

To the uninformed, “second-lowest” must count as a powerful point to put on behalf of an already poorly-funded university sector, facing further funding cuts, based on data drawn from an impeccably independent source. Such claims have rhetorical force, and make for handy media headlines – even in cases where the factoid is an OECD figure that refers to incomplete four-year-old (2013) data.

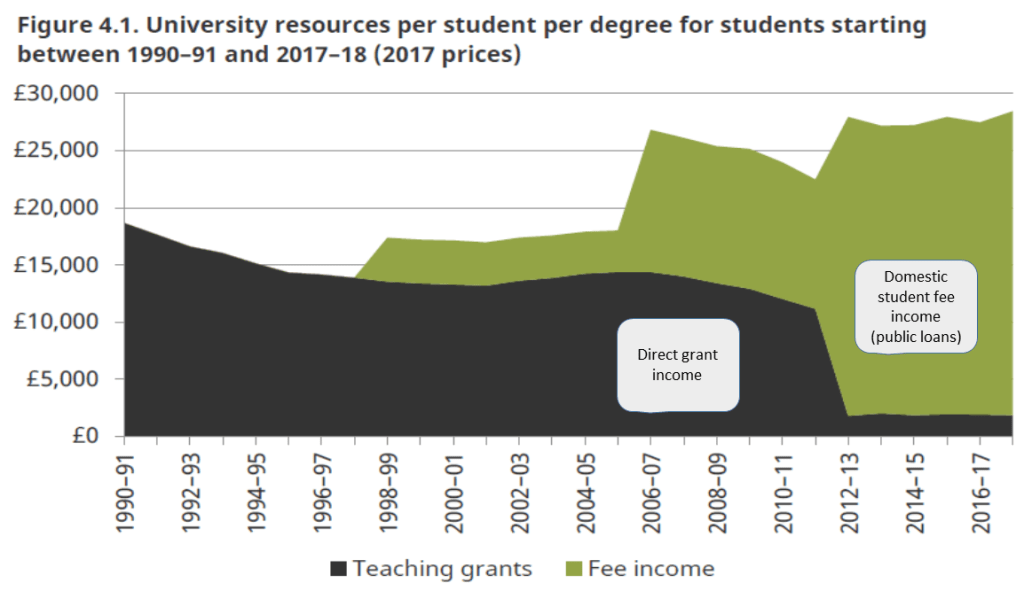

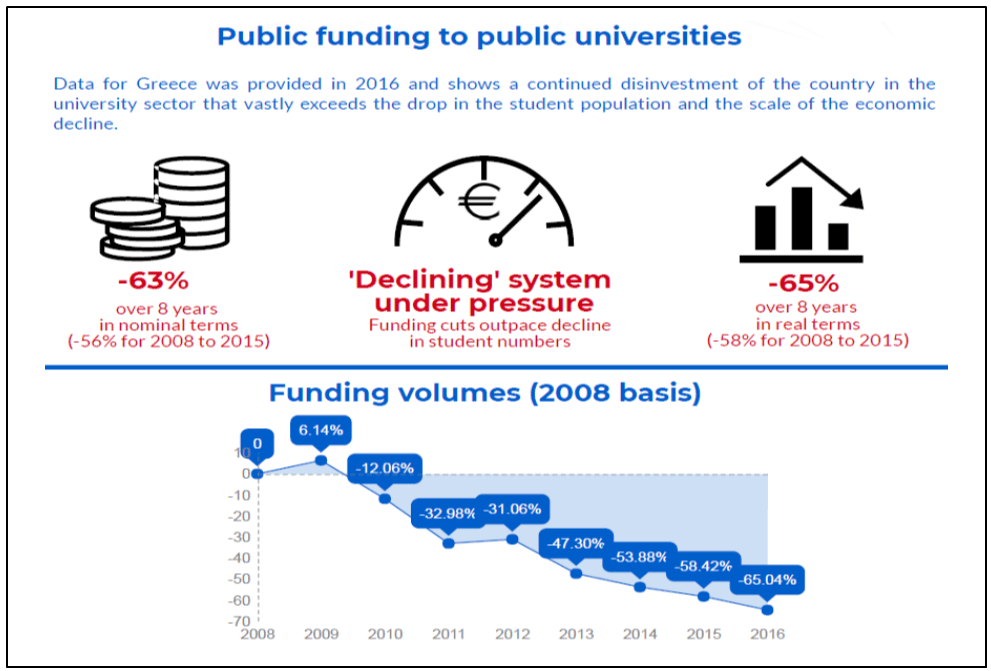

But apart from the problems just outlined, such claims from sector leaders imply that no-one who tracks Australian university finances was aware that in English universities, student loans all but replaced teaching grants in 2012 (see Figure 1 below). Or that in 2015, it became clear that OECD reporting classed UK loans as “public” and Australian loans as “private” (the problem has now been addressed – see Chart 7). They also imply that no-one who compares Australian university funding across the OECD was aware of the sharp declines seen in Greece since the 2008 financial crisis (Figure 2).

As I outlined in June, there are some caveats to Australia’s unusually high spending growth. The main one is that it reflects very high rates of enrolment growth. Over 2010-2016 the number of Australian tertiary students rose by 50% – even faster than total revenue (36%) in the OECD’s 2019 report. So, revenue per student declined, as the OECD average level rose over 2010-2016. But, this wasn’t due to stronger revenue growth elsewhere in the OECD. Just low OECD average revenue growth of 9% and even lower average enrolment growth of 3%.

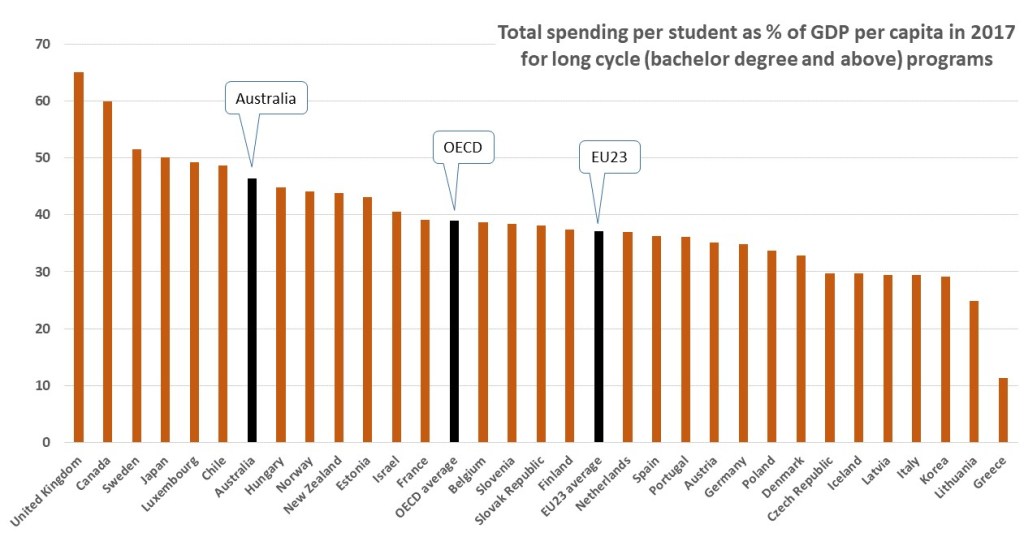

From this, a plausible concern is that course quality in Australian universities must have suffered more than elsewhere, due to our decline in revenue per student. However, in the latest OECD report, total spending per degree-level student in purchasing power parities (including R&D spending) remained well above the OECD average in 2017. Chart 9 shows Australia spending more than US$23k per student per year, against an OECD average figure of less than $18k and an EU average of just over $17k.

With spending per student as a share of GDP per capita, it’s a similar comparative story. Chart 10 shows Australia spending 46% per degree-level student (including R&D). This was comfortably ahead of the OECD average (39) and the EU average (37) in 2017.

Chart 11 shows that for total spending per tertiary student (degrees and diplomas, this time excluding R&D spending), it’s also a similar comparative story. Here Australia spends over US$14k per student in purchasing power parities, compared with EU and OECD averages of over $11k. (The gap in the Australian figures of $23k and $14k in Charts 9 and 11 is consistent with domestic data, which indicates that universities invest surplus revenue from international students in research more than in teaching.)

Local claims of low, flat or falling levels of spending, on the basis of a single metric, often reflect what is sometimes called “policy-based evidence“. Despite years of relatively strong spending growth, Australia’s “bottom of the OECD” status has been a constant theme and a key meme in the sector’s under-funding narrative. But it doesn’t present a realistic view of the “iceberg” of Australian expenditure. And it ignores the tougher realities faced by many other tertiary systems over the past decade.

The sector’s latest budget submission didn’t refer to OECD data at all. Sensibly, its case focuses on domestic data alone. This will always be more current and more relevant for government planning purposes. Perhaps in the 2020s the Australian folklore will fade. If the inconvenient truths outlined here gain credence, the apparent consensus among sector leaders may finally falter, in the face of so much disconfirming data.

Unreliable international comparisons won’t make future policy debates better informed. A good first step would be for our sector’s funding advocates to resist the urge to read each new technical report as a morality play about decades of local funding decline, while more enlightened OECD peers have kept investing.

In sum, let’s not rely so heavily on cosmopolitan impressionism. Particularly if it’s based on a single slice of the smorgasbord of statistical data the OECD provides. As a tool for telling the world how cash-strapped we are, “final public spending as a share of GDP” has been a fabulous way to make a “poor first impression” without proving much at all. But the sector’s “decline and fall of funding” story is past its use-by date. As standalone metrics, such claims should be dropped from expert commentary and formal advice to policy-makers, into our collective “Can’t Regard As Proof” bin, where they belong.

Update, October 2021

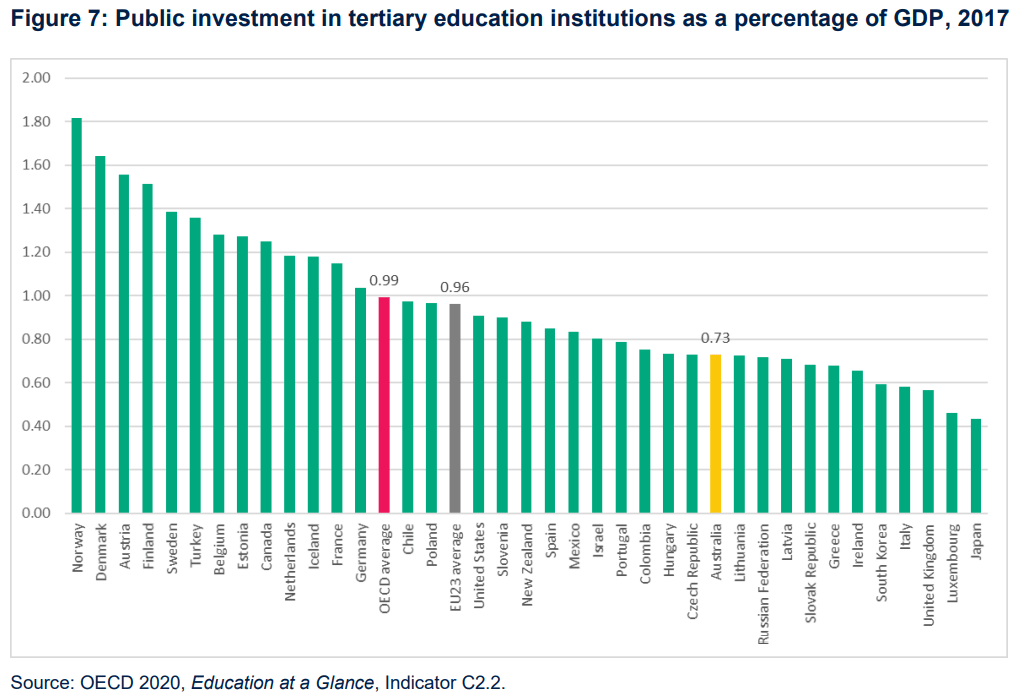

As seen in its latest Higher Education Facts and Figures report, Universities Australia has stayed on-script with OECD comparisons for tertiary spending: “In 2017, Australia’s total investment – public and private – in tertiary education institutions as a share of GDP was above the OECD average and the fourth highest … However, Australia’s public investment (Figure 7) in tertiary institutions as a share of GDP was amongst the lowest in the OECD – ranked 26 out of 37 countries. Australia’s public investment was 0.73 per cent of GDP in 2017 compared to an OECD average of 0.99 per cent of GDP.”

On this Chart 12 view, Portugal is ranked higher than Australia. However Chart 13 repeats the point that rankings based on public investment as a share of GDP leads to flawed comparisons. And leaving GDP growth aside, Chart 8 showed earlier that if Australian HELP loans are included (in what the OECD calls initial public spending) our rate of government investment was above the OECD and EU averages at 1.1% of GDP and a world away from that of Portugal’s 0.7%. Finally, Chart 4 showed that over the period 2005 – 2016, final public spending growth of 49% in Australia ran well ahead of OECD and EU average growth, while in Portugal it declined by 15%.

Notes

Since posting, I’ve updated minor details and added Charts 11 and 12.

In the June post I recalled how my first peer-reviewed journal article on this topic was pilloried in The Australian newspaper in 2016. It was framed as “an extraordinary attack” on sector leaders, experts and colleagues for their apparent “misuse” of OECD data. As outlined in Diary of an Academic Infidel, an informal complaint by one of my University of Melbourne colleagues led the Journal to reverse its publication without explanation and then refuse all appeals to republish.

In the years since, despite posting updates of its case in The Conversation, the sector’s narrative has continued much as before. In future posts, I’ll look at the wider question of debate quality within universities and the merits of free exchange on controversial topics.